According to this rather lengthy video, Rolex is dropping hundreds of smaller Rolex “dealer” outlets and instead creating Rolex megastores in “prime” locations such as London (!!!) and Manhattan (!!!).

It would appear that the main reason behind this is that Rolex wants to protect their brand by limiting the number of outlets, dropping smaller stores (regardless of relationship longevity) so that they can control the whole “Rolex buying experience” and provide their customers with the proper treatment with fine ambience, better-trained staff and so on. Also, these larger stores can carry the extensive Rolex range that a smaller store couldn’t.

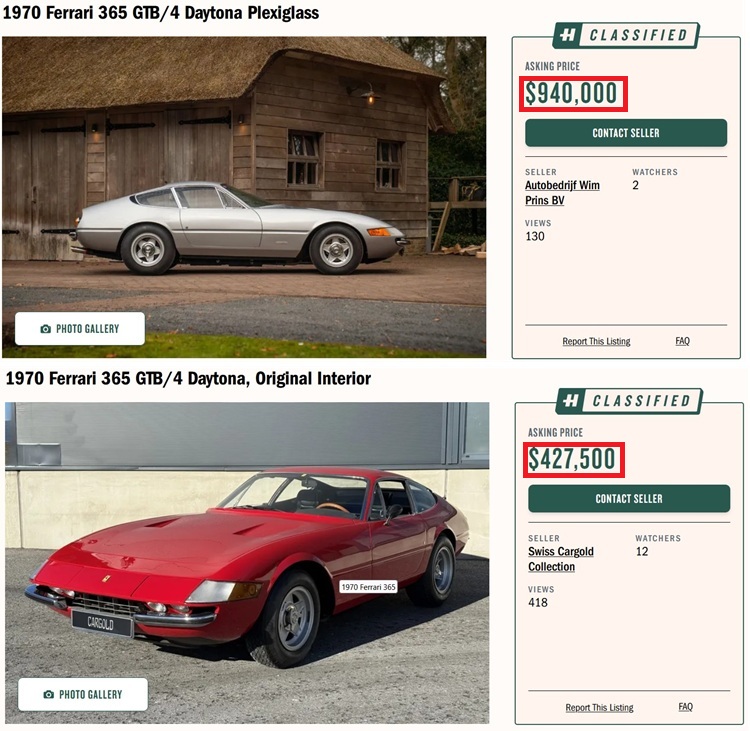

It all sounds well and good, except that the actual reason, it seems to me, is that during the sales spike caused largely by the Great Covid Panic of 2020, the people who really made money weren’t Rolex themselves but the profiteers who bought their watches and resold them on the “grey” market — and Rolex, like Ferrari, wants to keep as much of the market to themselves. (Same tactics, different product.)

Of course, there’s nothing wrong with what they’re doing. As long as there are people willing to pay the inflated prices of their products, then good luck to them.

My own personal take on the thing is that I’m indifferent because (regardless of any lottery winning) I would never be a Rolex sucker buyer in the same way as Ferrari would forever be outside my list of automotive choices (except maybe a Dino, although given the current price list of same… nah, never mind). Sorry, I’m no longer impressed by brand names, especially when the brand’s “value” is artificially pumped up by fools and suckers with more money than sense. And even more so when the brand operates in a commodity category like watches.

And finally, I happen to think that those big, blocky things like the Submariner are just… ugly. I’m not a scuba diver so I’ll never need one, and anyway, there are other watches just as good for half the price and a tenth of the Rolex attitude (once again, see: Ferrari dealers).

A pox on all their houses.